Free Quote

Use the form below to request a free home insurance quote. We’ll shop for the best coverage options and rates for you.

Request a Home Insurance Quote

Buying the right homeowners insurance policy isn’t as easy as it used to be. Some companies offer better coverage than others, some exclude or limit things you would expect to be covered, and some carriers have non-renewed or are no longer issuing new policies in the state. As a result, finding a great home insurance rate with a reputable carrier has become more difficult in recent years.

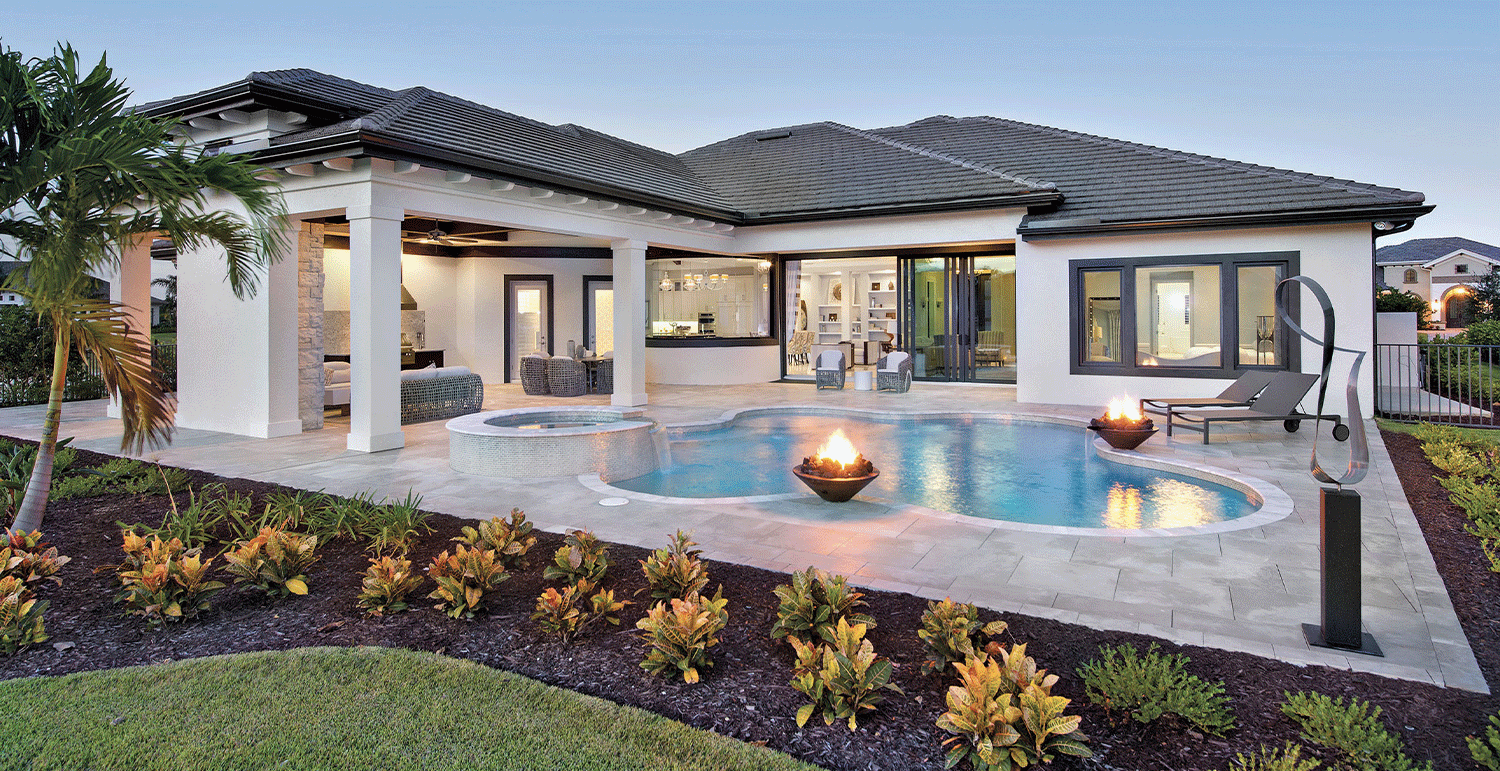

Typically, a house is the most valuable asset a person owns. So, it is very important that it is protected and covered by insurance. Remember replacing or repairing your property is just a part of your need for protection as a home owner. Your Port Charlotte home insurance policy should also be carrying the right amount of liability coverage to ensure that you and your family are covered in case of a disaster.

Port Charlotte is prone to windstorms and hurricanes, that’s why house owners here must have a reliable homeowners insurance to protect their property.

In addition, expensive home amenities and high-valued personal belongings contained in your home should also be considered for additional coverage. So, take time today to ensure your policy affords the protection you need should the unexpected happen. Call our office to speak directly with an agent or use our website’s convenient contact form to have a representative explain your options for homeowner’s insurance.

We’ll work with you to understand your personal needs, and help to find a great rate with a company that will be the best fit for your families home.

Compare homeowners insurance quotes from every top insurance company.

Your information is completely secure and never shared.

With hundreds of satisfied South Florida clients, Ezzi Insurance Advisors is here for you & your family.

Frequently Asked Home Insurance Questions

Free Home Insurance Quote

Ensure your property’s value long-term. We’ll shop for the best coverage options and rates for you.